How I Identify a stock for Investment.

How I Identify a stock for Investment.

Finding the Needle in Haystack

My this Post is the cumulative learnings I have acquired from various Investment Managers ranging from Warren Buffet, Charlie Munger, Philp Fisher, Li Lu, Terry Smith, Chuck Akre, Mohnish Pabrai, Nick Sleep, Guy Spier, Tom Gayner, Nick Train, Peter Lynch, Jack Bogle, Rakesh Jhunjhunwala, Utpal Seth, Managers at Nalanda capital, Sumeet Nagar, Sanjay Bakshi, Bharat Shah, Saurabh Mukherjea, Ramdeo Agarwal, and many other Giants of the Financial Markets.

Here I will lay down the Five framework approach which I use and this framework has proved it’s dominance for the above giants. Therefore, I feel going forward it will immensely help me and you all reading this.

Let’s begin.

1. Circle of Competence.

Warren Buffet uses this extensively and I wonder even if a day goes by where he doesn’t mention his circle of competence to others. Circle of competence as per my understanding is to have a deep understanding of what you know and what you don’t know.

Now this doesn’t mean only understanding the product which the company sells, but it involves understanding of the business economics i.e. how will the profitability look decades later. This is the key in understanding any company you invest into.

I have literally ZERO understanding about working of a computer or how a software works but I have a fair understanding that 10 or 20 years later definitely people would be wearing Chappals, people would have to eat something, people will be wearing jewelry. Hence I tend to find companies in such industries which are easy to understand and those whose future cash flows can be roughly estimated.

Similar approach was used by Peter Lynch when he used to spot companies going to a grocery store or a supermarket which lead to 29% CAGR investment returns during his investment management journey.

2. Opportunity Size.

Rakesh Jhunjhunwala starts his investment looking at the size of opportunity also Bharat Shah of ASK group says you have to first determine the size of the pond i.e the opportunity, then look for the fish i.e individual company. In his book ‘Of Long Term Value & Wealth creation’ he says, “The real issue is figuring the size of pond, while often, the debate in investing world is about size of the fish”

Infosys would not have been Infosys if there was not an explosion in foreign opportunity due to internet. Titan would not have been Titan if there was no formalization in Jewelry industry. Similar is the case with all the successful companies.

Now look where the opportunity went to ZERO. For example Kodak was one the most powerful companies in the world but when Figi introduced low cost high quality cameras the opportunity for Kodak died and as kodak did not change based on opportunity, the company became bankrupt. Here also take a look how Circle of Competence has played a role; If you knew the photography making industry thoroughly and you were invested in Kodak, you could have sensed the threat of Figi cameras and sold Kodak shares.

3. Quality of Business and Management.

First take a look at this award winning Motilal Oswal advertisement

As you would have seen in the video, cheap quality never works and will not work even in case of businesses. So let me explain the most important aspect of investment.

Quality of Business:

The quality of business is determined by how much Returns on Capital Employed (ROCE) a business generates and the reinvestment rate of such capital. Now ROCE in simple terms is the money I have invested in the business and the money which i get out of business at year end. For eg: I start a vadapav business with initial capital of Rs.100 and at the year end I have received 200 rupees total and after deducting expenses my profit that is Sales-Expenses is 100 rupees, now I will say that ROCE of my business is 100% (100/100 x 100%).

Hence for investment I look for businesses which have ROCE of more than 20% sustained for more than 10 years.

Now comes the reinvestment of capital part which most investors fail to understand. Take a company like Castrol Limited

The ROCE has been consistently above 20% for many years but the pays out all of its profits in form of dividends, hence the reinvestment rate of Castrol is very Low. You can link this point with the 2nd point I mentioned which is the size of opportunity, if the size of opportunity for Castrol was high it would have reinvested it’s profits back into it’s business. I avoid such Companies.

Take a look at Asian Paints Limited

Asian Paints also has earned more than 20% ROCE for more than 10 years but the reinvestment rate for Asian paints is High. It pays average 30% of profits as dividends and reinvest 70% profits back again into the company. Such are the companies I generally invest in.

Hence Two key takeaways: 1) Return on Capital Employed should be more than 20% for 10 consecutive years and 2) Reinvestment rate should be high.

Quality of Management

The People in the company are the spine of the company. If there was no Dhirubhai there would be no Reliance, similarly is case with JRD Ratan Tata- Tata Group, Narayan Murthy- Infosys, Deepak Parekh and Aditya Puri- HDFC group and many other such cases.

The important qualities which Warren Buffet looks for in the management :

Hence, no matter the growth prospects and do hell with the energy, if a company has Shady promoter who has involved into Insider trading or has High political connection dependence, pays less taxes, doesn’t answer to shareholders grievances, I completely avoid such companies.

One more aspect to look for is the promoter holding in the company. I generally I’m skeptical to invest in companies having less than 50% promoter holding. This called as eating your own cooking. I also avoid cases of promoter pledging their shares because once a down cycle hits the market and the promoter doesn’t pay the debt the bank will offload such holding.

4. Growth and Longevity of Growth.

This point mainly overlaps the opportunity size point. I like a company where it’s current market share as compared to the overall market size is low. Hence such companies have an exponential growth phase ahead of them. Michael Mauboussin in his paper ‘Competitive Advantage period’ speaks about the similar characteristic of business where the business has a huge runway ahead and the growth is not cyclical in nature.

Here I will take the example of Relaxo Footwears Limited

The sales for Relaxo has increased from 554 crores 10 years back to about 2500 crores in 2021 which leads to 13% CAGR in sales. This has mainly happened due to 2 reasons: 1) Eating the market of Unorganized players in cities like Ulhasnagar, kolhapur, and many other small footwear manufacturers. 2) Eating the market of it’s rivals like Bata Limited.

Now considering the market size still remaining to be acquired, Relaxo has both Growth and Longevity in Growth.

5. The Price you pay.

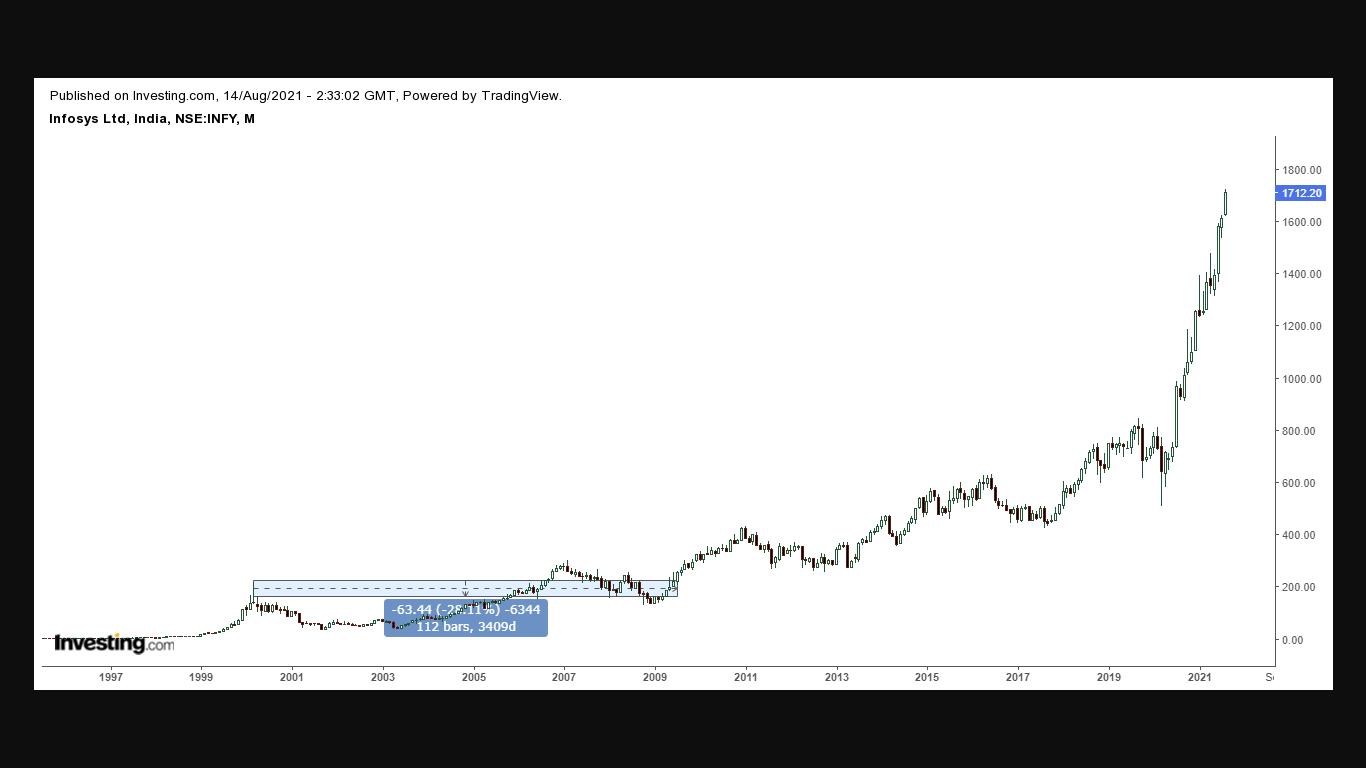

This is indeed one of the toughest part of investing into any company. No matter the Growth or future prospects, the price you pay is ultimately going to decide your investment returns. Take a look at chart of Infosys from 2000-09

The price barely moved above the high made in march 2000 that is during the tech boom. Now the business was growing, ROCE was great, promoter Narayan Murthy was one of the best leaders in his industry, yet we the investors would have not made any money (except for the dividends). Hence this is the outcome of overpaying for a stock although it is good company.

The trick which I use is to get more quality than the price I’m paying. When in 2015 Food regulator banned Maggi the product of Nestle the share dipped, but the people who knew that major revenues of Nestle comes from Baby Milk powder and not from Maggi products or confectionery bought Nestle at lower valuations and they may not sell for next 20 years. This is the trick which Terry Smith, the manager of UK based Fundsmith has used extensively. Similar is the approach which Warren Buffet used in buying American Express during the Salad Oil scam and Charlie Munger used during buying Wells Fargo in 2008 crisis. He maintains a watchlist of companies which he understands and then once the opportunity arises he just pounds on them. As he always says ‘Opportunity comes to a prepared mind’.

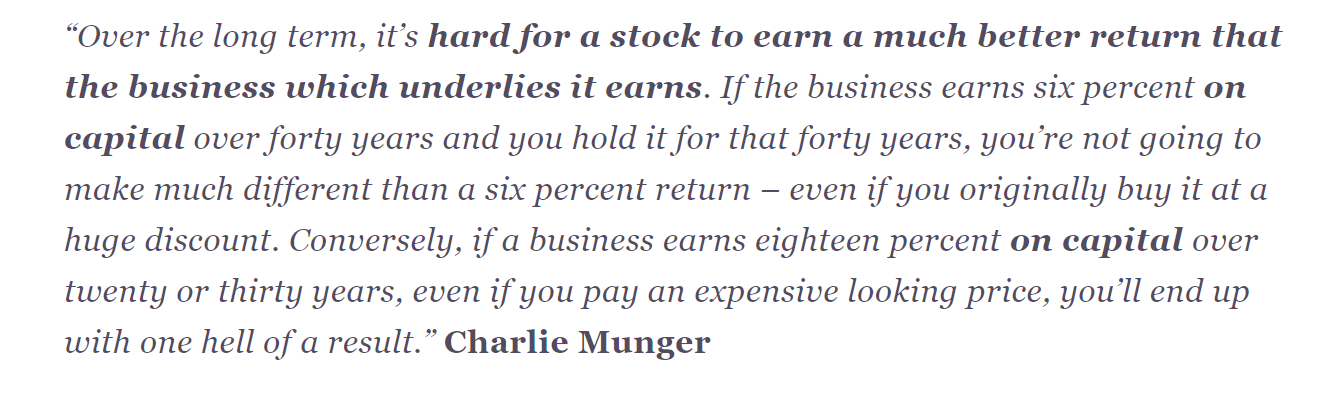

Also if the ROCE is High, the company will replicate the same in it’s long term share price. Read what Charlie has to say:

Hence, you should be ready to pay a reasonable price but avoid paying a high price in crazy bull market.

Other key metrics.

Some key points which I consider while looking at a business:

Debt to Equity of less than 0.5. I don’t want growth at the expense of overleveraging the balance sheet.

Low equity dilution. If there is constant dilution of equity it is a red flag.

Pledged shares of the promoter. Ideally promoter should have zero pledged shares.

Less Capital Intensive industry. The companies having huge capex requirement will be the most to suffer in economic downturn. Hence I generally avoid those.

Having too many subsidiaries. If the company has subsidiary involved in the similar kind of business then it should be avoided.

Contingent Liabilities. Company should have almost Nil contingent Liabilities.

So to summarize the points:

1. Circle of Competence.

2. Opportunity Size.

3. Quality of Business and Management.

4. Growth and Longevity of Growth.

5. The Price you pay.

(published on 14th August 2021)